If you plan to be in business you'd better have a Business Plan. If you plan to start a small business this tool can be the difference between success and losing everything. If you think this Business Plan tool is expensive wait til you see how expensive it is to NOT have a well thought out and written business plan.

If you are considering starting or buying a business it's a good idea to have the best tools. It may cost you a few bucks but it could be a cost that saves you many, many thousands of dollars.

A good business planning tool will also allow you to compare options from a consistent platform.

I think the best

Business Plan Software on the market today is

Business Plan Pro . (Yes, this is an affiliate link and we get a few cents if you buy it but, hey, give us a break, we did the research).

The best part about this software is it's intuitive and you don't need an MBA to operate it. The Standard edition is all most people ever need. It's a product that has been around for many years and it's very practical and efficient to learn.

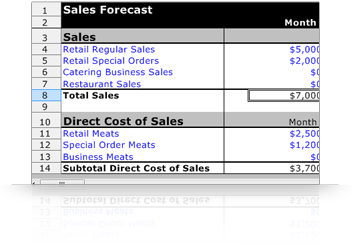

As you can see the layouts are clean and easy to understand.

If you are going to get into business you need a plan that is logical, well thought out and proven. Trust me, if you go to your banker with a professional business plan your odds of getting financing improve dramatically. A plan like the one

Business Plan Pro produces will be a requirement for any SBA loans that you apply for or pursue.

Here's a few fatal mistakes a good business plan can help you avoid.

The best time to have a business plan is before someone asks you to see it! Get ahead of the curve...get your plan.